Verifi specializes in dispute management, aiding sellers in revenue retention and cost reduction from banks.

Contents

Recommended Articles

What is Payment Orchestration? A Complete Guide for Businesses in 2026

Payment orchestration is a software layer that connects your business to multiple payment service providers, acquirers, banks and other financial services through a single platform, it allows you to manage transactions across various partners and optimises success...

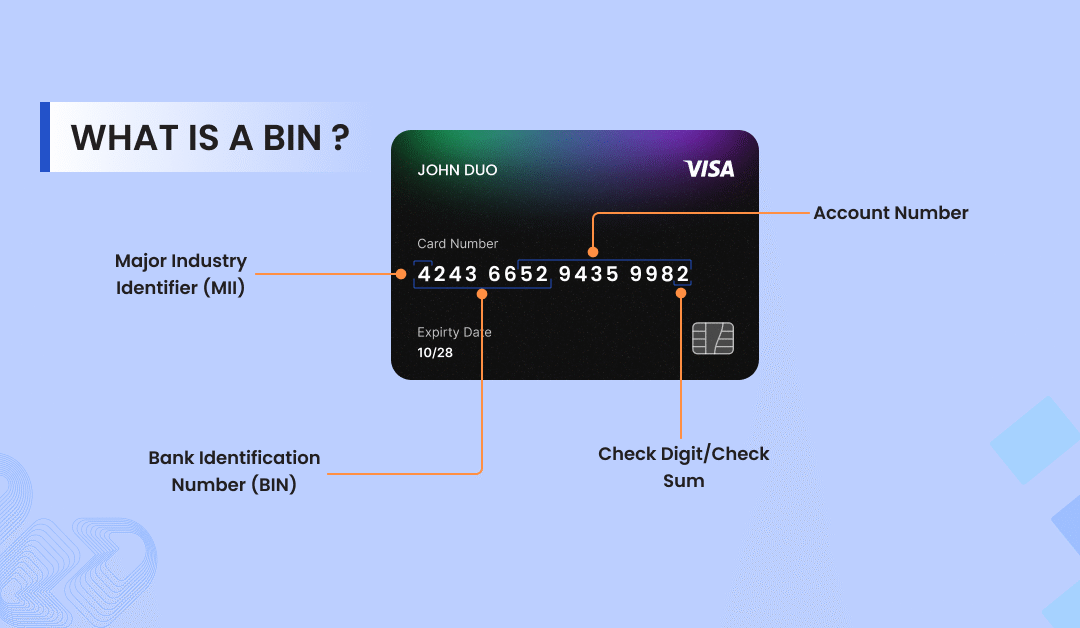

What is BIN in Card Payments? A Guide Every Merchant Need

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

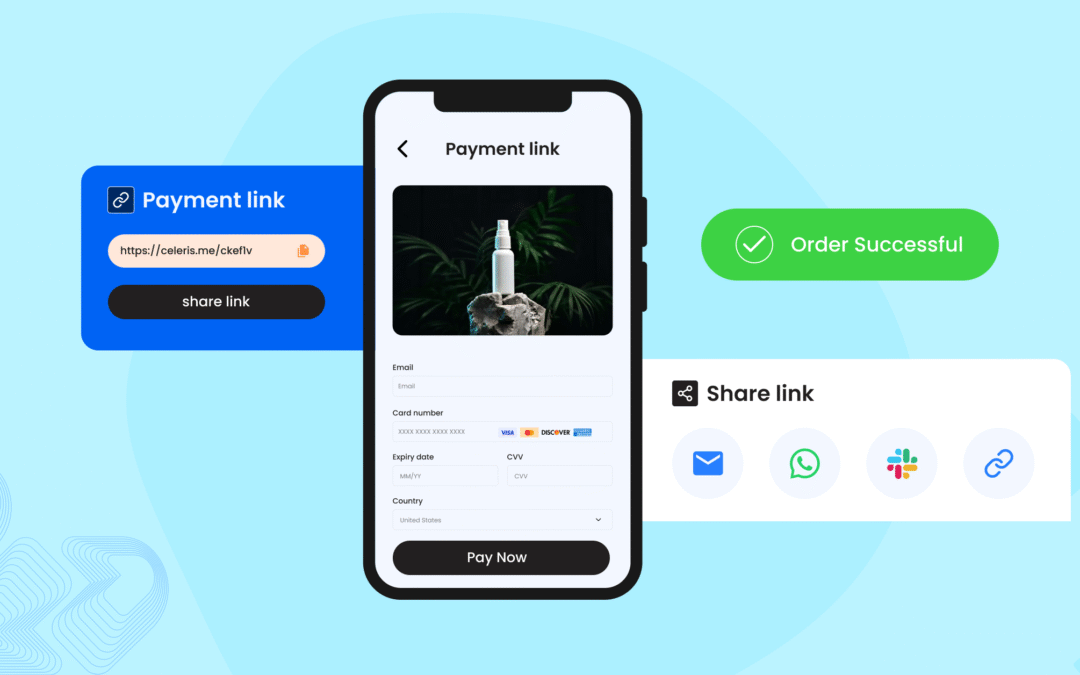

Pay by Link: A Smarter Way to Accept Payments in 2025

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

Share This Post

Payment tokenisation is a security technology that can reduce online payment fraud by up to 60%. For years, businesses in sectors such as e-commerce and banking have utilised tokenisation to secure payments and safeguard customer data.

With the continuous rise of cyber threats, it has become essential for businesses to safeguard customer data without compromising the user experience.

That’s where payment tokenisation can help you in securing customer data by replacing sensitive payment information with a unique, non-sensitive equivalent known as a token. This token is useless to hackers, enhancing security while maintaining a seamless payment process.

This guide explains the fundamentals of payment tokenisation, including its benefits, mechanics, and role in simplifying PCI DSS compliance. Whether you are a fintech professional, an e-commerce merchant, or an investor, this article provides a comprehensive overview of payment tokenisation.

What’s in this guide:

-

What are Payment tokens?

-

What is payment tokenization, and how does it work?

-

The Benefits it offers to businesses

-

Real-world examples of tokenized payments

-

How to choose the right solution for your business.

Contents

What are tokens?

A payment token is a randomly generated string of characters that acts as a substitute for sensitive payment data, such as a credit card number, bank account details, or a Primary Account Number (PAN).

Unlike encrypted data, which can be reversed with a decryption key, tokens are irreversible and cannot be reverse-engineered to reveal the original information.

Because they hold no intrinsic value, tokens are useless to fraudsters even if intercepted. This makes them a highly effective tool for protecting data during storage, transmission, and retrieval.

For example, a credit card number like 4523-3734-3762-7328 might be tokenised into A23D-CB64-H5Y3-G7H8. This token represents the customer’s card details for a specific transaction and has no value outside of that transaction. For recurring billing or one-click checkouts, tokens can be stored securely in a token vault without exposing the original card data, allowing businesses to process future payments & subscription renewals without compromising on speed and security.

What is Payment Tokenization?

Payment tokenisation is a data protection process where sensitive payment information, like a credit card number, is replaced with a randomly generated string of characters called a “token.” As explained above, this process ensures the original data is never exposed during a transaction, significantly reducing the risk of data breaches and fraud.

How Does Payment Tokenisation Work?

Here’s a simplified breakdown of the payment tokenization process:

-

Initiating a Transaction: A customer enters their card details at checkout or taps their card on a payment terminal.

-

Token Generation: A tokenisation service provider, such as Celeris, captures the real card details and generates a unique token to replace them. For example, the card number “4512-1243-5678-8765” becomes “XT96-KLP9-JH52-GH90.”

-

Token Storage in Secure Vault: The newly generated token is stored in a secure token vault managed by the provider, while the actual card details are isolated.

-

Verifying the Transaction The token is sent through the payment gateway to the issuer bank for authorisation. Only authorised parties, such as the merchant and bank, can link the token back to the original data in the vault.

-

Completion of Transaction: Once the transaction is approved, the token can be stored for future use, such as for recurring subscriptions or one-click checkouts, eliminating the need for customers to re-enter their details.

What’s crucial here is that even if a hacker intercepts the token, it holds no value without access to the tokenisation vault or decryption methods. This is why tokenisation is a superior security method to traditional encryption methods.

Two types of tokenization payment

With Celeris, merchants can use two main types of tokenisation for payments:

Payment with CVV: If a user opts to “save card details” for a one-time transaction, their card number, expiry date, and name are tokenised and stored in the celeris token vault. For future purchases, the customer only needs to enter their CVV to complete the payment, creating a frictionless checkout experience.

Payment without CVV: For recurring billing, Celeris securely transmits card information to the issuer bank, which generates a unique ID for that card. This ID is stored and used for future recurring payments without requiring the customer to re-enter their CVV or other details, ensuring a seamless and secure subscription experience.

An Example of tokenization

Imagine you’re buying a pair of shoes online and you entered your credit card details, but before storing the sensitive credit card details, data protection technology (tokenisation) will replace the data with a randomly generated string of numbers or characters called “tokens” like “A1B2C3.” Even if hackers can breach the merchants’ side, this token cannot be used outside of that purchase, keeping your details safe and secure.

Tokenization vs. Encryption: A Detailed Comparison

-

Tokens are non-sensitive, which means even if a hacker breaches, he won’t expose cardholder details.

-

Unlike encryption, tokens cannot be mathematically reversed without access to a secure vault.

Traditional payment methods store data like credit card numbers in plaintext or encrypted formats, prime targets for cybercriminals. With tokenization, this data is stored as a form of a tokenized version (like 123456XYZ789), ensuring that even if a hacker intercepts the token, it’s useless for them without access to a secure vault provided by a payment gateway (like Celeris). By doing so, businesses can reduce the risk of breaches while maintaining seamless payment processing.

Top 5 Benefits of Payment Tokenization for Businesses

Enhanced Security

Using tokenization, one of the most significant benefits is the high level of security it provides, replacing the customers’ sensitive payment data like card details or payment details with secure tokens, increasing the layer of protection and safeguarding both your business and your customers.

Fraud Prevention

Studies showed that businesses using data protection technology (Tokenization) have significantly reduced online payment fraud by up to 60%. Unlike raw payment data, tokens cannot be reused on other platforms or transactions. This makes it nearly impossible for hackers to exploit stolen payment tokens, offering an added layer of security in every transaction.

Streamlined Payment Processes

For industries like eCommerce, tokenization has emerged as a game-changing solution that also simplifies operations:

-

By using tokenization services, you don’t need to process customers’ payment details repeatedly; the details will be stored in the form of tokens, which helps to reduce friction and provide a frictionless checkout experience to customers.

-

Improves user experience by facilitating faster transactions and reducing declines caused by flagged sensitive details.

Marketplaces and Platforms

Online marketplaces and platforms that allow other vendors to sell their products on their platforms need a payment system to manage transactions across various sellers. With a white label payment gateway, they can provide a unified, secure and seamless payment experience while reflecting the platform’s branding.

Simplified Compliance

Tokenization streamlines merchants’ compliance with PCI-DSS regulations by ensuring that sensitive data is not stored with the merchant. Instead, tokens are used for transactions, and merchants only have to manage the security of tokens and the key, which reduces the scope and cost of compliance audits.

Improved customer Trust

As we’ve already explained, payment tokenization is important in today’s growing digital commerce. When shopping online from an e-commerce store, customers may be concerned about the security of personal information like card or payment details. By implementing tokenisation into their payment flow, businesses can demonstrate their commitment to protecting customers’ data, which helps them build trust and loyalty with customers.

What Types of Businesses Should Use Payment Tokenization?

Tokenization is not only for e-commerce; it offers significant advantages to various businesses that handle sensitive customer data, transforming security across industries.

Here’s how:

E-commerce: Tokenization helps e-commerce businesses take the example of merchants using the Celeris global checkout solution or one-click payment solution. Tokens ensure that customers’ card details are not captured or stored on the merchant’s servers, significantly reducing the risk of online payment fraud.

Subscription-Based Businesses: Tokenization can help businesses that offer subscriptions for their products or services. These businesses need to provide a seamless recurring billing experience to customers to increase retention. Tokenization ensures that sensitive information is replaced with tokens for ongoing payments. It provides a smooth recurring payment experience without requiring customers to provide their payment details repeatedly. This creates a frictionless customer payment experience, leading to higher transaction conversion rates.

Healthcare: Hospitals and clinics use tokenization to secure patient payment portals. By replacing sensitive data with tokens, healthcare providers can comply with HIPAA regulations while offering a smooth billing experience.

Travel & Hospitality: Airlines and hotels use tokens to store payment details for future bookings. For instance, a frequent flyer program integrated with Celeris can tokenise card details for hassle-free reservations and additional last-minute upgrades or enhancements.

Fintech: Peer-to-peer payment apps and digital wallets rely on tokenisation to protect user data. Celeris’ solutions enable secure transactions without exposing bank account or card details.

Expert’s Views and Market Research on Payment Tokenization

Bankinfosecurity: Research conducted and published on 19 February 2025. Mastercard’s chief digital officer Pablo Fourez, told Information Security Media Group that fraud rates are seven times higher online than in physical stores, as criminals exploit exposed card numbers. He said that shifting to tokenisation protects businesses from financial losses and safeguards reputation and customer trust. ” Tokenization can reduce the fraud rate by 60%,” Ramakrishnan said.

Juniper Research: Based on the research conducted and published in 2022 by Juniper Research, Hampshire, UK – 18 July 2022: A new study from Juniper Research has found that the total number of tokenized payment transactions will exceed 1 trillion globally by 2026, rising from 680 billion in 2022. This represents a growth of 58% over the next 4 years. It attributed this growth to the rise of ‘one-click’ solutions, such as Click-to-Pay, that use card-on-file tokenization to store a customer’s payment credentials, enabling them to auto-fill their checkout details and complete transactions via a single click.

Asked

What is payment tokenization?

Payment tokenization data protection technology that replaces sensitive data (e.g., credit card numbers) with randomly generated tokens, which are useless to hackers and ensure secure transactions.

How does network tokenization work?

What are tokens, and how are they created?

Let's Connect

Just a few quick details. Our team will reach out to explore how our platform fits your payment stack and objectives.

Talk with one of our payment experts

Ready to elevate your business to new heights? Schedule a call with our experts to discuss your unique needs and uncover tailored solutions. Don’t let questions linger – seize the opportunity to pave your path to success!

Winner !

Best use of data analytics, MPE 2025

Best Payments Orchestration Solution, MPE 2024