Verifi specialises in dispute management, aiding sellers in revenue retention and cost reduction from banks.

Contents

Recommended Articles

What is BIN in Card Payments? A Guide Every Merchant Need

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

Pay by Link: A Smarter Way to Accept Payments in 2025

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

The Complete Guide to 3D Secure Authentication

Online payment fraud isn’t slowing down. As digital commerce scales, so do the risks of online payment fraud, according to a Juniper Research market…

Share This Post

Payment orchestration is a software layer that connects your business to multiple payment service providers, acquirers, banks and other financial services through a single platform, it allows you to manage transactions across various partners and optimises success rates, reduces costs and improves the customer experience.

This guide will explain everything business owners need to know about payment orchestration: how it works, its core features, and how to select the right platform to transform your business’s payment operations.

No time to read the full article? Connect directly with our experts to learn everything you need to know about our orchestration solution: Book a Call

Contents

Why Do Merchants Need Payment Orchestration?

Customers today expect seamless checkout experiences regardless of where they shop or how they pay, and the payment infrastructure most merchants are running simply wasn’t built to keep up with all these requirements.

The rising complexity of payments

Europe is a prime example of a fragmented payment market. Customers in the Netherlands often use iDEAL, customers from Germany may prefer SEPA direct debits or PayPal, and credit cards are dominant in the UK.

Managing these local preferences often requires integrating with different local providers. A merchant selling across the EU might end up with five or six different payment integrations just to offer the “standard” payment methods in each region. This creates a technical nightmare for maintenance and reconciliation.

Why single-PSP setups fail more often

A single PSP setup creates a structural vulnerability that goes beyond the obvious downtime risk. Approval rates are not consistent across geographies.

A global PSP with strong acquiring relationships in North America may have limited local presence in Italy, Spain, or Poland, which means transactions from those regions are processed cross-border, and issuers decline at a higher rate. The merchant sees a drop in conversions without ever knowing exactly why.

When that single provider experiences downtime, which every provider does at some point, there is no fallback provider available to you, and you are left with no choice until they are live again. Every transaction during this period fails to process, resulting in revenue loss.

Key Problems Orchestration Platforms Solve

-

Technical Overhead: One API connects you to various providers worldwide, eliminating the need to build and maintain separate integrations per provider or other tools, saving you time and money.

-

Revenue loss from provider failure: If a provider goes down, transactions automatically reroute to a backup based on rules you define in advance, not during an incident.

-

Excessive processing costs: Routing rules can direct each transaction to the most cost-effective acquirer for that card type, currency, and region, systematically reducing cross-border interchange fees over time.

Core Benefits of Payment Orchestration

-

Higher Approval Rates: Routing transactions to local acquirers who understand regional banking nuances significantly reduces false declines.

-

Lower Costs: Smart routing can direct domestic transactions to local providers, which avoids higher cross-border interchange fees.

-

Simplified Compliance Centralising payment data helps streamline the management of PCI DSS and GDPR requirements.

How Payment Orchestration Changes Merchant Payment Infrastructure

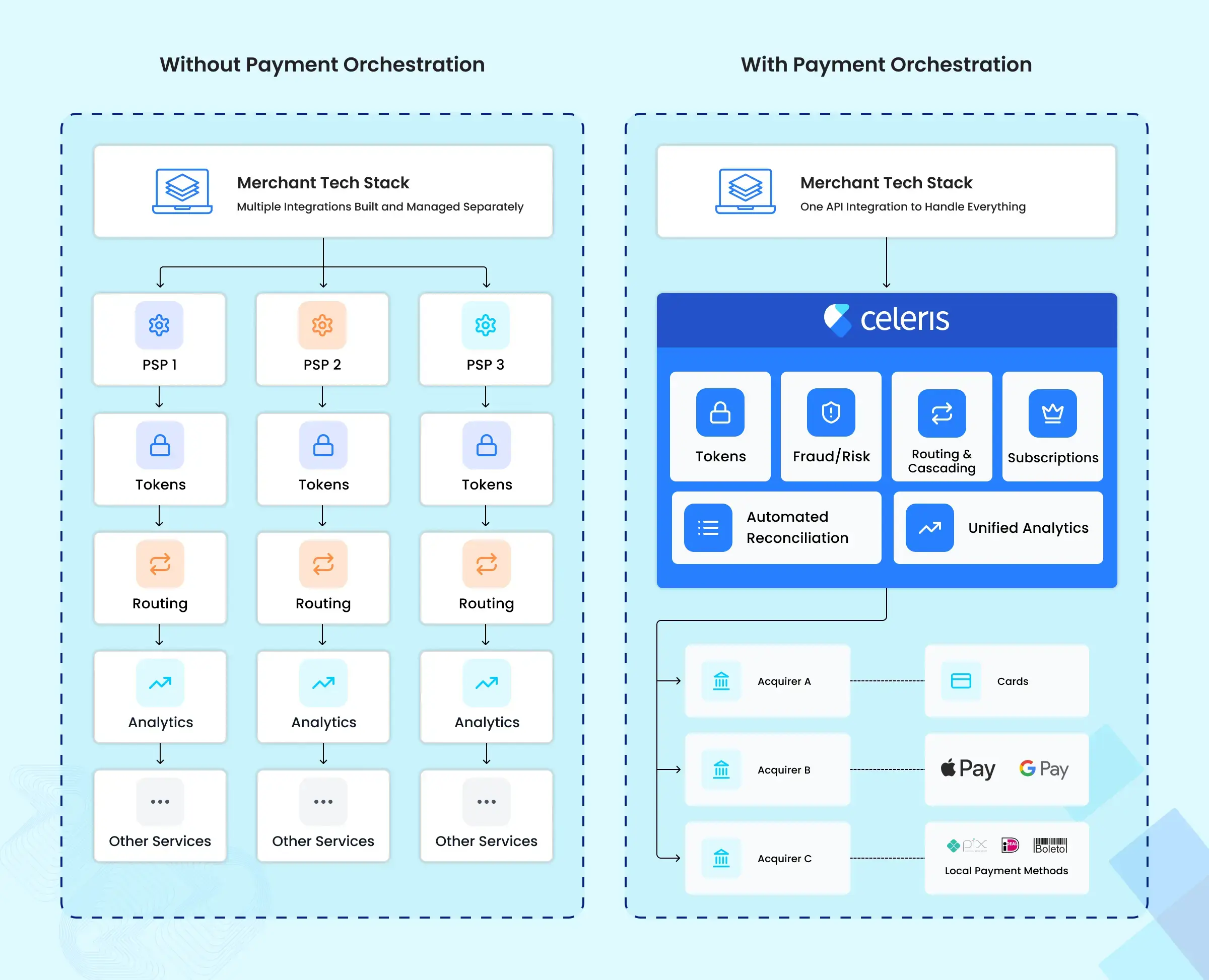

Payment orchestration changes how merchant payment systems are connected and managed. Instead of sending transactions directly to individual providers, payments pass through an orchestration layer that decides where and how each transaction should be processed.

Payment Infrastructure Without Orchestration

In a traditional payment setup, merchants connect directly to each payment provider. Card processors, gateways, and local payment methods all require separate integrations.

Each provider runs on its own logic. Reporting is split across different dashboards. When a payment fails, the transaction stops. There is no automatic retry through another provider.

Fraud checks operate separately from routing decisions. Payment data is scattered, making it harder to see which providers perform well in different regions. Adding new payment methods takes time and development effort.

Payment Infrastructure With an Orchestration Layer

With payment orchestration, merchants use a single integration to connect to multiple providers. All transactions pass through the orchestration layer first.

The system decides where to route each payment based on location, payment method, and historical performance data. If a payment receives a soft decline, it is automatically retried through another provider.

Fraud checks are part of the same flow, helping balance security and approval rates. New payment methods can be enabled through configuration. Merchant can view all payment activity in one place, making performance easier to track and optimise.

How Payment Orchestration Works?

To understand how a POP works, it’s important to know its 2 core components.

Main Components

-

Connector Library: Pre-built integrations to hundreds of PSPs, fraud detection tools, and local payment methods.

-

Routing Engine: The logic centre that decides where a transaction should go based on criteria you define, such as

currency, card issuer, transaction value, or risk score. -

Token Vault: A secure database that stores customer-sensitive card data as tokens. This ensures you control your customer data, not your PSP.

-

Rules Engine: The interface where merchants configure routing logic. For example: “If a transaction is over €100 and from France, send it to Provider A.”

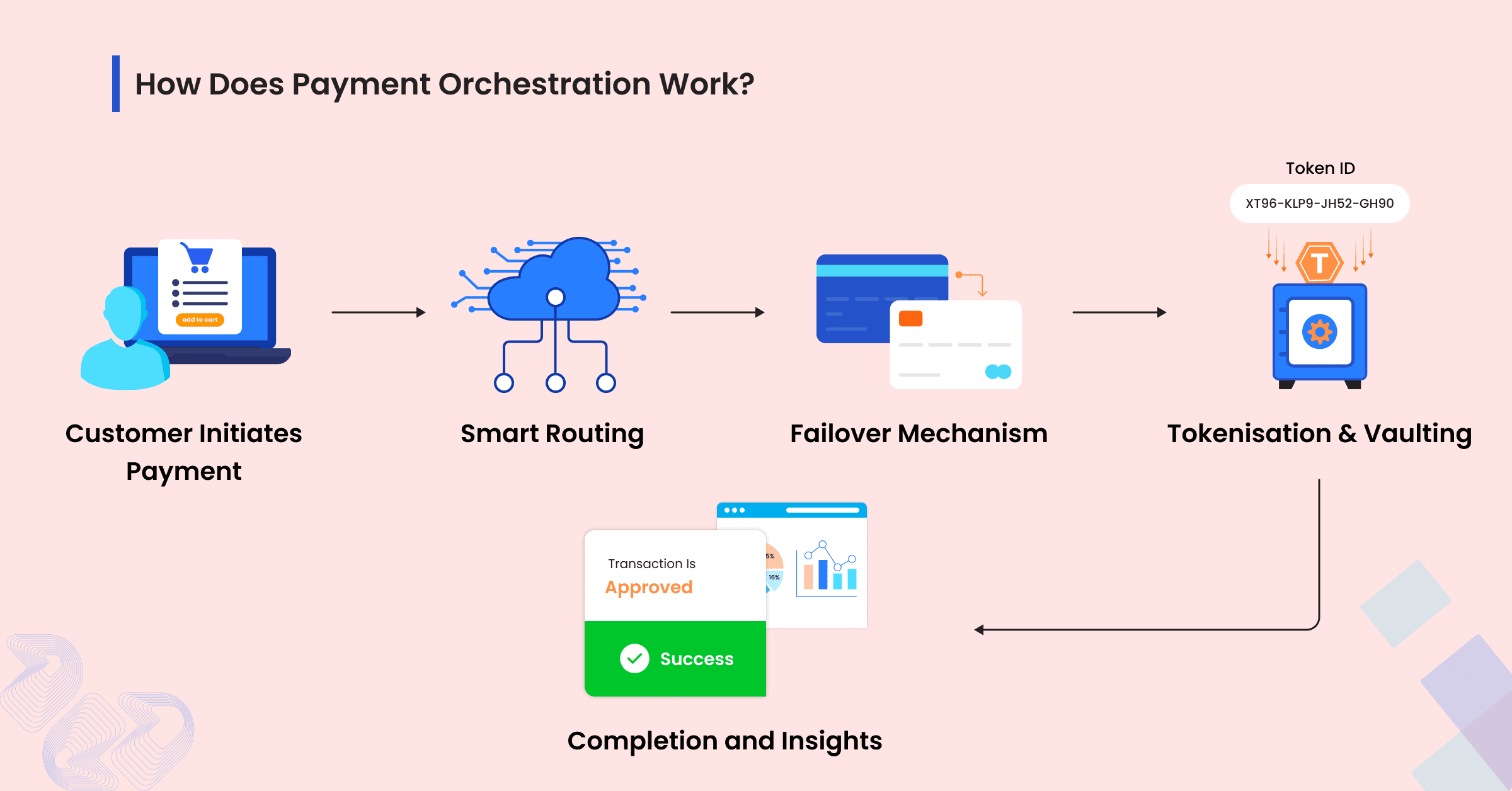

Example of a Transaction Flow

-

Checkout: A customer enters their card details on your checkout page.

-

Tokenisation: The POP captures the payment data and replaces it with a secure token. Your servers never handle the raw card information.

-

Routing: The routing engine identifies the card as a Visa issued in Germany. It applies a merchant-defined rule: “Route German Visa cards to the local German acquirer.”

-

Processing: The transaction is sent to the selected German acquirer for authorisation.

-

Failover: If the German acquirer is unavailable or declines the transaction, the POP instantly retries it with a backup provider.

-

Confirmation: The payment is approved, and the customer receives a confirmation message.

Key Features Of Payment Orchestration That Improves Overall Payment Performance

Smart Routing and Cascading

This is the core of orchestration. You can configure rules to route transactions based on the lowest fees and the provider with the highest approval rate for that specific transaction type. If a gateway goes down, cascading ensures the transaction automatically “falls over” to a backup provider, which potentially saves your revenue.

Tokenisation and Secure Vaulting

Payment orchestration separates customer data from the payment provider; for example, our orchestration platform separates payment data from the payment processor. By using a platform-agnostic token vault, you retain ownership of your customer’s card data. This allows you to switch providers without asking customers to re-enter their details, which is a critical feature for subscription businesses. (You can also read: What is payment tokenisation)

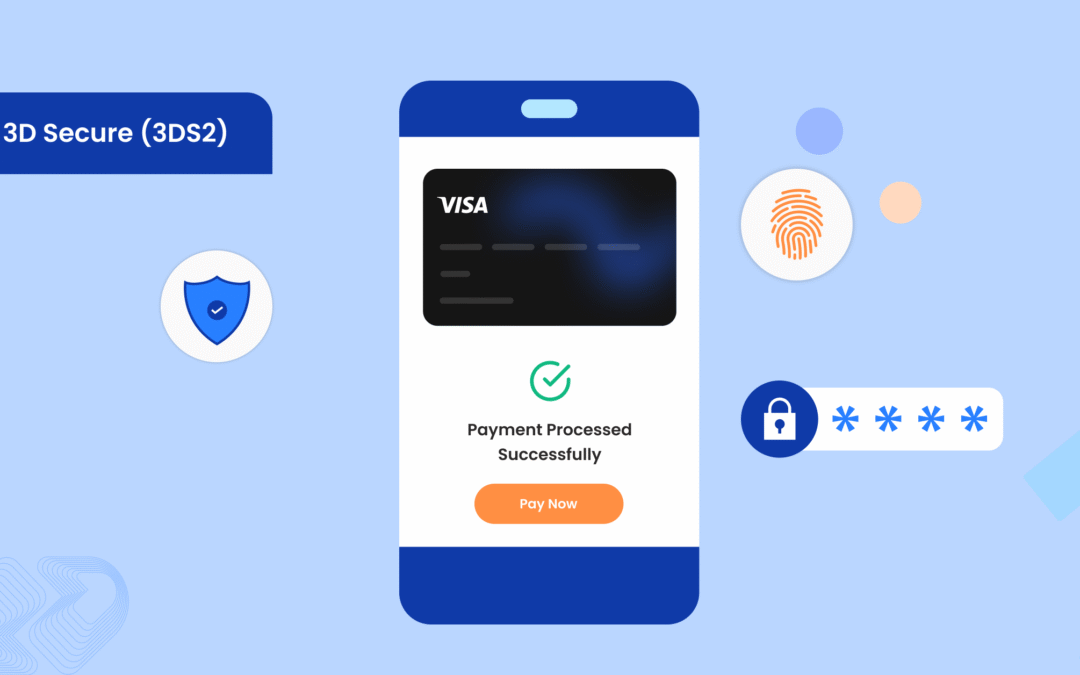

3DS2 and SCA Optimisation

Strong Customer Authentication (SCA) is mandatory for most online payments in Europe, but it can add friction during the checkout process. An orchestration platform can identify when exemptions apply (such as for low-value transactions or trusted beneficiaries) and request 3D Secure authentication only when necessary, which helps maintain high conversion rates.

Chargeback Management

The orchestration platform also provides a unified dashboard for viewing and managing disputes across all your payment providers. At Celeris, we integrate with Ethoca & Verifi early alerts and chargeback help for chargeback scoring for potential chargebacks. With our advanced dashboard, you can set up rules to automatically refund a disputed transaction before it escalates into a formal chargeback, which protects your merchant accounts by keeping the chargeback ratio lower. Wanted to know more visit how to choose the right chargeback solution.

How Orchestration Platforms Support Regulations and Compliance Requirements While Maintaining Performance.

PSD2 and SCA Explained Simply

The Revised Payment Services Directive (PSD2) mandates Strong Customer Authentication (SCA) for most online payments in Europe. While necessary for security, it introduces steps that can lower conversion rates.

Reducing Friction and Supporting Exemptions

The Second Payment Services Directive (PSD2) mandates multi-factor authentication for most online payments in Europe to enhance security.

An orchestration platform manages the 3D Secure flow centrally. It can signal to the bank when a transaction is eligible for a frictionless flow, allowing the authentication to occur without requiring customer interaction. To know more about it, you can visit 3DS Exemptions.

GDPR and Secure Data Handling

Handling European customer data requires strict compliance with the General Data Protection Regulation (GDPR). Leading orchestration platforms are built with “privacy by design,” ensuring data is encrypted, stored within the EU where required, and processed according to compliant data processing agreements.

Supporting Local EU Payment Methods

To succeed in Europe, you need to offer more than just Visa and Mastercard. A POP allows you to easily enable local payment methods, including:

-

iDEAL (Netherlands)

-

SPEI (Mexico)

-

PIX (Brazil)

-

SEPA Direct Debit (Eurozone)

-

Apple Pay, Google Pay

The Business Case: ROI, Costs and Key Metrics

Calculating ROI from Approval Rate Uplift

For mid-market and enterprise merchants, even a 1% increase in approval rates can mean significant revenue. For instance, if your current approval rate is 85% and orchestration increases it to 86% through local acquiring, that 1% lift translates directly to your bottom line. For a business processing €10 million annually, its €100,000 in recovered revenue.

The above data is just an example; actual outcomes depend on many factors and vary widely based on industries.

The Impact of Local Acquiring on Costs

Cross-border interchange fees are often 1% to 3% an orchestration platform allows you to use local acquirers in the customer’s region. For example, processing a French card through a French acquirer is significantly cheaper and more likely to be approved than processing it through a US-based acquirer. This can result in a significant reduction in processing fees.

Important KPIs to Monitor

A unified dashboard like celeris allows you to track key metrics across all providers:

-

Authorisation Rate: The percentage of approved transactions.

-

Recovery Rate: The percentage of transactions saved by failover routing.

-

Blended Cost per Transaction: The total cost after routing optimisation.

How to Choose the Right Orchestration Partner

To understand how a POP works, it’s important to know its 2 core components.

Operational Checklist

-

Support: Do they offer a dedicated support team?

-

Uptime: Is the infrastructure reliable enough to handle peak trading periods?

-

Incident Response: How quickly do they communicate gateway outages?

Legal Checklist

-

Data Sovereignty: Does the platform comply with GDPR regarding where data is stored?

-

PCI DSS: Is the provider Level 1 PCI DSS compliant?

-

Portability: Do you own the tokens, or are they locked to the provider?

Technical Checklist

-

API Quality: Is the documentation clear, and is there a sandbox environment?

-

Connectors: Does the provider support the specific PSPs and methods you need?

-

Flexibility: How granular are the routing rules?

Commercial Checklist

-

Transparency: Are the pricing models clear, with no hidden volume fees?

-

Contract: Is the onboarding seamless? (CelerisPay offers seamless onboarding to get you live in weeks, not months.)

Why Celeris is the Best Choice for Your Business in 2026

Celeris is a leading and award-winning payment orchestration solution provider in Europe, working with 200+ merchants and large-scale businesses.

Key Features of Celeris

-

60+ Global Integrations with seamless onboarding

-

AI-Based Smart Routing for better payment success rates.

-

Bank-Level Security with PCI DSS compliance and fraud tools.

-

Real-Time Reporting Dashboards for actionable insights.

-

Dedicated Support Team to guide you through implementation

Whether you’re an ambitious startup or an enterprise, Celeris’s advanced features grow with your business, making it the ultimate choice for payment orchestration in 2025.

Challenges of Payment Orchestration

As all of you already know, nothing is perfect, and understanding the hurdles of payment orchestration helps you while choosing the payment orchestration provider for your business. Here are some challenges:

Complex Rule Management: Setting up efficient routing rules requires initial planning and ongoing refinement to maximise performance.

Cost of Implementation: While orchestration reduces long-term costs, some integration solutions available in the market can charge higher upfront costs.

Provider Dependencies: Despite failover mechanisms, poor performance from PSPs can still create challenges in payment flows.

Security Requirements: Handling sensitive financial data comes with the responsibility of maintaining PCI DSS compliance and robust fraud prevention mechanisms.

To avoid these challenges, partnering with a provider offering seamless onboarding and strong support is crucial.

With Celeris, you won’t face any of the challenges mentioned above, as we have built orchestration solutions that integrate easily with your existing payment flow and are available at an affordable cost compared to others. Our support team is always available to address any questions or issues that may arise. Additionally, we adhere to all necessary security measures, including PCI-DSS Level 1 Compliance and other regional security standards.

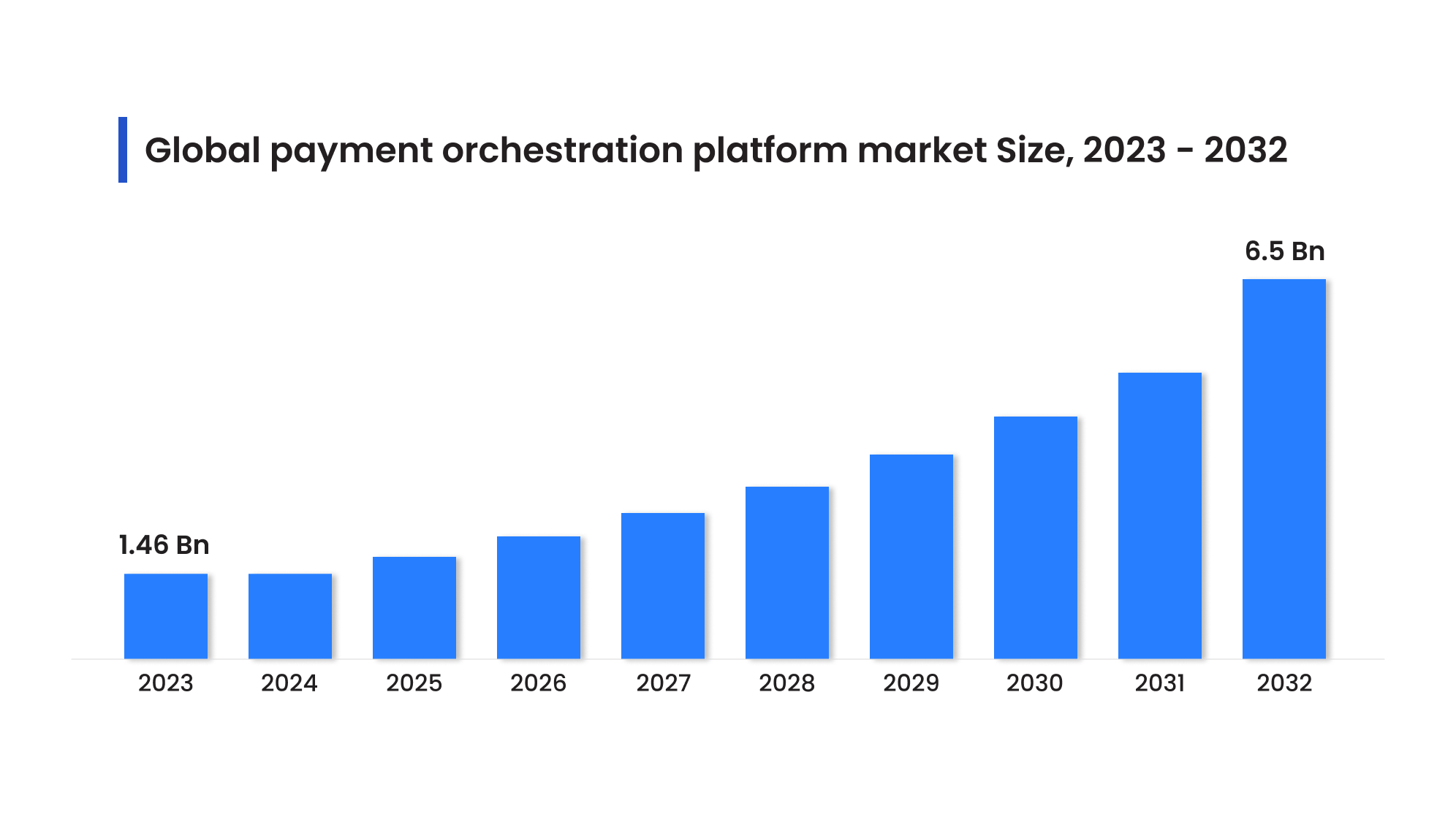

Market Size & Future Trends in Payment Orchestration

Payment trends and the industry are changing rapidly. Based on research, payment orchestration is expected to surpass revenues of $ 6.1 billion by 2030, highlighting its position at the forefront of innovation.

Source

Payment Orchestration Trends in 2026

Here are some payment orchestration trends in 2026 and beyond:

AI-Driven Routing: Expect more intelligent algorithms that learn from transaction history to predict and optimise payment success in real time.

Blockchain Integration: Decentralised payment methods are becoming mainstream, and orchestration platforms will soon integrate solutions like cryptocurrencies.

Advanced Fraud Detection: Real-time fraud prevention tools powered by machine learning will become essential features of orchestration platforms.

Embedded Finance: Beyond payments, orchestration platforms will integrate lending, insurance, and financial services for complete user journeys.

Getting Started with Payment Orchestration

Three steps to get started with Celeris today:

Book a Call With Team: Discover how our orchestration solution works, ask your doubts, share your requirements, and understand top to bottom what you’ll get from us.

Integration Support: Our onboarding team will ensure a smooth and fast setup.

Optimise Payments Instantly: Go live in a week, not in months.

Asked

What is payment orchestration?

Payment orchestration is a software layer that connects a merchant to multiple payment providers, allowing for centralised management and optimisation of all transactions.

How does payment orchestration work?

What are the benefits of payment orchestration?

How is payment orchestration different from a payment gateway?

How does smart routing work?

What type of industries benefits the most from payment orchestration?

How does payment orchestration handle failed transactions?

How do I choose the right payment orchestration platform?

How much payment orchestration platform costs ?

How does payment orchestration handle failed transactions?

Does payment orchestration support recurring payments?

What are the risks of using payment orchestration?

Why do approval rates differ between countries?

How does a POP connect to PSPs?

What is required for PSD2/SCA compliance?

How long does integration take?

Let's Connect

Just a few quick details. Our team will reach out to explore how our platform fits your payment stack and objectives.

Talk with one of our payment experts

Ready to elevate your business to new heights? Schedule a call with our experts to discuss your unique needs and uncover tailored solutions. Don’t let questions linger – seize the opportunity to pave your path to success!

Winner !

Best use of data analytics, MPE 2025

Best Payments Orchestration Solution, MPE 2024