Verifi specialises in dispute management, aiding sellers in revenue retention and cost reduction from banks.

Contents

Recommended Articles

What is Payment Orchestration? A Complete Guide for Businesses in 2026

Payment orchestration is a software layer that connects your business to multiple payment service providers, acquirers, banks and other financial services through a single platform, it allows you to manage transactions across various partners and optimises success...

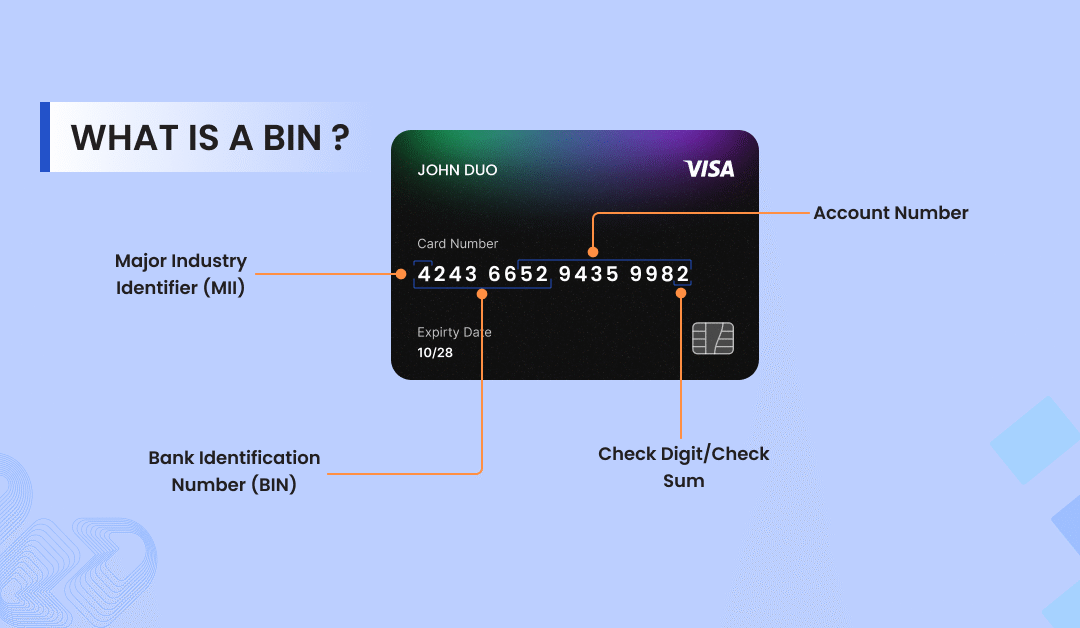

What is BIN in Card Payments? A Guide Every Merchant Need

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

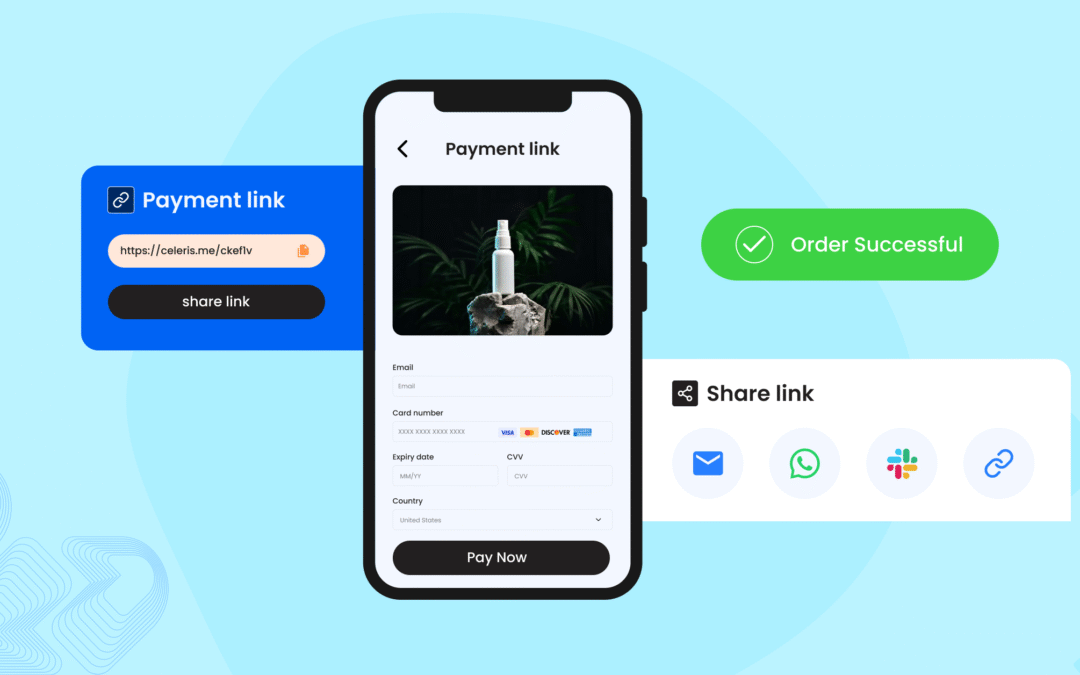

Pay by Link: A Smarter Way to Accept Payments in 2025

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

Share This Post

Contents

Introduction

“Banks have been the torchbearers of providing financial services practically, since time immemorial. Consumers have relentlessly relied on them, trusted them and have been dependent on them for various monetary operations. However, it wasn’t long ago that various financial crises hit the society, one after the other, shaking the said trust in these institutions. With the advent of technology, there have been path-breaking innovations in nearly every existing sector and the financial realm is no exception. One of the most prevalent results of this innovation is the rise of modern fintech firms that are catering to a wide range of customers with the provision of streamlined financial services, backed by the latest technology. The following article analyses the possible competition between the said traditional banks and modern fintechs – Are they “really” competing or can they join forces to build a more robust financial services sector?”

Fintechs and Banks – What are they?

Fintech is a term that combines the words “finance” and “technology.” It essentially creates financial comfort which is produced by merging modern technology and the provision of financial services. This allows consumers to access the said financial services with ease. Because of its convenience and mobility, we are witnessing a revolution in the financial sector, with a rise in the use of technology for financial services rather than the banking system. Furthermore, due to the widespread and necessary use of the internet, regulatory authorities can readily track and regulate these transactions, ensuring that “Fintech” is used efficiently. The Modern Fintech revolution had essentially begun in the late 1990s when E-commerce and the Internet were being born. By the advent of the 21st century, technology was actively incorporated in the backend systems of financial institutions to digitize banking services. However, the demand for Fintech firms grew steeply after the 2008 crisis, when the consumers looked for better and more trustworthy solutions when compared to traditional banks. Traditional Banks, on the other hand, are licensed financial institutions. They are permitted to receive and maintain monetary deposits and provide loans to individuals or businesses. However, as the banking sector has developed in contemporary times, they can provide a host of services including but not limited to wealth management, investment strategies, safe deposits, currency exchanges, and corporate dealings. Mostly, every jurisdiction would have a central regulatory bank that would look over all of the above.

How are traditional banks being disrupted by emerging modern fintechs?

A McKinsey report showed that during the first few months of COVID-19, the usage of mobile banking channels saw a surge of 20-50%. It is highly predicted that these numbers are not going down even after things get back to normal. Customers are also showing an increasing inclination towards digital banking and more flexible solutions, preferring multi-channel interactions with remote human assistance only in the cases when it is necessary. The increasing demand for speed, efficiency, and flexibility compel financial service providers to integrate technology into their services and provide for a frictionless and more user-friendly experience. Modern Fintechs have essentially bridged this gap between what traditional banks could offer and what a modern consumer expects. The Business Research Company reported that the fintech market worldwide was valued at $127.66 billion in 2018 and is expected to grow at a yearly growth rate of 25%, at least till 2022. This explains the fact that the top 50 Fintech firms in Europe have raised over $16.8 billion in venture capital funding.

Traditional Banks vs. Modern Fintechs – The difference

Credit must not be entirely taken away from traditional banks as well since they have evolved drastically by incorporating AI, ML, data analytics and even acquiring some Fintechs to enhance the quality of their operations. Both banks and fintechs are essentially financial institutions as well – so what is the difference between modern fintechs and banks? There are specific markers where both these types of institutions tread starkly contrasting paths. Let us examine how traditional banks and modern fintechs are reshaping the financial services ecosystem.

Structure and Purpose of Functioning

Fintechs and Banks are differentiated by their general approach to their operations. Modern Fintech solutions are developed by recognizing a market gap, whereas legacy institutions such as banks serve a larger audience. Legacy banks are primarily concerned with risk management, whereas modern fintech organizations are concerned with the overall customer experience. The central idea thereby creates a difference in their structures. Fintechs are generally more customer-centric and aim to streamline complex processes. Their operating models are leaner, free of legacy issues which enables them to innovate and rebuild systems with ease. On the other hand, traditional banks have to necessarily cater to the regulatory framework and require a larger workforce and infrastructure to function. They are essentially more process-oriented which makes the introduction of newer services or products more cumbersome for them.

Customer Experience

As has been made clear, Fintechs are upcoming private entities that are focused on providing a more customer-centric and personalized user experience to their clients and customers. Physical contact or communication is kept to a minimum in their operations, prioritizing agility and accessibility. Legacy banks, however, majorly work on physical communication which compromises convenience. Although some people would still prefer them due to their long-drawn history of being credit providers who have sovereign insurance for their liabilities and a comparatively more resilient business model which prioritizes security.

Communication

The Banks which have made themselves familiar with new-age technologies have also focused more on better UX designs which ensures a more seamless experience for their customers. Modern Fintechs have a more augmented communication pattern in this regard where they constantly focus on swifter transactions and possibly 24×7 access, customer service, and consultancy. The remote access feature of their operations makes it necessary to have hassle-free communication with consumers.

Perspective on Technology

New-age technologies like machine learning, artificial intelligence, cloud computing and analytics are at the heart of Modern Fintech operations. They depend heavily on automation and reducing the risks involved in e-transactions. Banks, on the other hand, are grappling with legacy infrastructure, although there is a substantive effort on their part to digitize their operations. However, the existing infrastructure shall be an obvious deterrent in a complete shift to digital mechanisms.

Potential Markets

Due to the flexible nature of Fintechs, they carry more associated risks with themselves. Banks are strictly regulated and thus, minimizes the risk involved with them. However, this also means that there is better growth potential in the Modern Fintech market, especially as it is quite young. Due to better mobile phone connectivity and E-commerce, Fintechs also register better penetration – still, the trust factor lies with the banks and it is quite a task to make all of their users shift to a completely digital platform.

Fintechs and Banks – Friends or foes?

Both Traditional Banks and Modern Fintechs work as financial intermediaries. On one hand, banks have existed for ages, while on the other, Fintechs are the result of modern innovation. Banks also have much larger deposits and are strictly regulated by government authorities. Modern Fintechs possess the capability of providing better services and catering to the needs of their customers.

The conclusive notion in this regard is that both these types of institutions need to work in cooperation with each other for the development of a more robust and accessible financial system. The collaboration will provide Modern Fintechs with a much larger user-base, with better regulation while the Banks would be able to augment their operations with the services of the latter. This essentially creates a win-win situation, combining innovation with trust to build a more secure digital financial future.

Let's Connect

Just a few quick details. Our team will reach out to explore how our platform fits your payment stack and objectives.

Talk with one of our payment experts

Ready to elevate your business to new heights? Schedule a call with our experts to discuss your unique needs and uncover tailored solutions. Don’t let questions linger – seize the opportunity to pave your path to success!

Winner !

Best use of data analytics, MPE 2025

Best Payments Orchestration Solution, MPE 2024