Verifi specialises in dispute management, aiding sellers in revenue retention and cost reduction from banks.

Contents

Recommended Articles

What is Payment Orchestration? A Complete Guide for Businesses in 2026

Payment orchestration is a software layer that connects your business to multiple payment service providers, acquirers, banks and other financial services through a single platform, it allows you to manage transactions across various partners and optimises success...

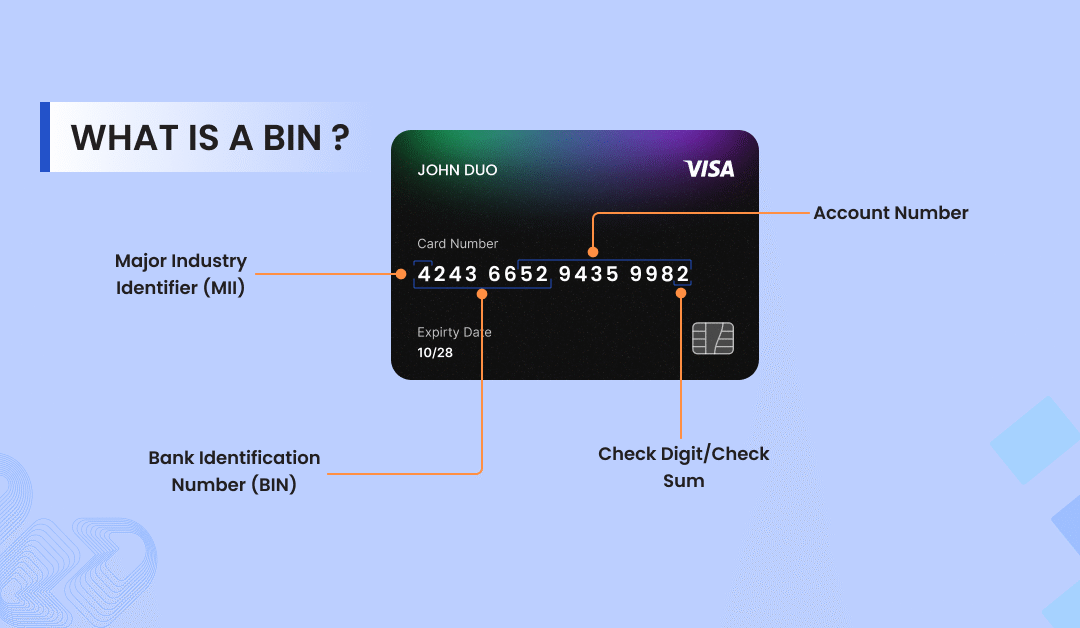

What is BIN in Card Payments? A Guide Every Merchant Need

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

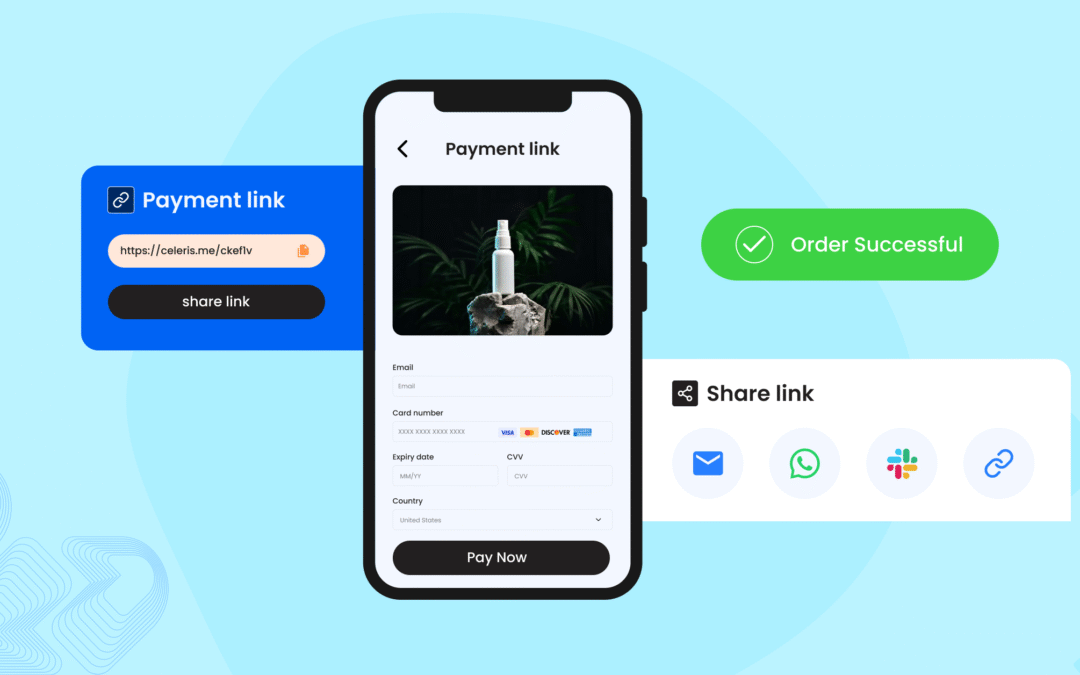

Pay by Link: A Smarter Way to Accept Payments in 2025

Most businesses today close sales through conversations, not just via websites or apps. Customers interact with your brand across various channels, including Instagram, WhatsApp, email, and live chat.

Share This Post

As we enter this new year still in the midst of a pandemic, it is vital for payment companies to foresee digital payment trends and plan ahead of time. The best way to predict customer patterns and preferences is to follow the current economy, the pandemic and of course innovations in digital payments. However, with the abundance of new payment tools, regulations and financing options it can be overwhelming to plan one’s next move for both merchants as well as payment companies. So we’ve broken down the most relevant changes and digital payment trends we expect to see in the payment industry this year.

Contents

Frictionless payments move towards Invisible payments

With the way things are currently going the future of the payments industry is undoubtedly moving from frictionless payments towards invisible payments. Payment companies have gone above and beyond to reduce customer friction at checkout, knowing that even a little bit of friction could lead to annoyance, second thoughts and higher cart abandonments. Once customers get used to frictionless digital payments, it’s near impossible for them to go back.

Frictionless payments can be defined as digital payments that occur seamlessly, with minimal pain points (like handling cash, entering PINs or wielding cards). Among frictionless digital payment options, mobile wallets are by far the most popular. The mobile wallet market exceeded USD 100 billion in 2020 and is expected to grow at more than a 20% CAGR between 2021 and 2027. Over the years we’ve also seen a shift in popularity from merchant-specific mobile wallets (e.g., Starbucks app, McDonald’s app) to merchant-agnostic mobile wallets (e.g., Google Pay, Apple Pay). Initially, this wasn’t the case as merchant-specific wallets would offer incentives and coupons that would draw in a larger customer base. However, more recently, merchant agnostic wallets have started offering incentives too allowing them to overtake merchant-specific wallets.

Invisible payments can be defined as digital payments that are made without any specific transaction-oriented interactions. The idea is to completely eliminate the need to provide any credentials for authentication, instead making use of only biometric data.

Amazon has definitely spearheaded the movement of the invisible payment, having implemented this technology at their Amazon Go stores. Customers with Amazon accounts simply scan a code at the store entrance, walk in and pick up the items they want to purchase, then they walk out without having to checkout manually. Cameras keep track of each individual’s purchases, placing every item in a virtual shopping cart that they automatically charge for when the customer leaves. Amazon has also introduced Amazon One which links cards to an individual’s unique palm print, allowing them to simply hold up their hand in front of a scanner to make digital payments. With the way things are going, invisible payments are going to be on a major rise in the payments industry this year.

Real-Time Payments

Real-time payments (RTP) are defined as the instant settlement of digital transactions between individuals and/or merchants without waiting for clearance. RTPs are facilitated through a digital infrastructure known as a real-time payments rail. It is important to understand that these are different from “fast payments” which happen through traditional payment rails. RTPs have been gaining a lot of recognition in the payments industry for several reasons- speed being the most obvious one. Another benefit is that real-time payment rails facilitate end-to-end communication, unlike traditional payment rails. Instead of information being exchanged solely from the payer to the payee, RTPs allow information to be exchanged both ways without exiting the payment system. The traditional payment rail’s fragmented communication process can impact business continuity as well as liquidity and risk management. Instant payment confirmation notifications, settlement finality and bilateral communication all result in a more efficient payment journey. So it comes as no surprise that recent US-based reports state that 130 financial institutions are going to implement RTPs in their existing infrastructures this year. This digital payments trend is definitely going to take the payments industry of 2022 by storm.

Buy Now, Pay Later (BNPL)

With the holiday season being the most expensive time for everyone, one of the biggest digital payment trends has been the ‘Buy Now, Pay Later’ option. This offers a low or 0% interest rate of micro-credit at checkout and is likely to become a great alternative to traditional credit cards. The market size of BNPL companies is over $2 billion globally and BNLP transactions have increased by 200% over the last few years. An Insider Intelligence report predicts that the industry will grow to $680 billion in transaction volume by 2025. Other studies show a 44% increase in conversion rates for merchants who provide BNPL options. Hence it’s crucial for players in the payments industry to be able to provide this as an option.

Open Banking

Payment industry regulations in Europe, as well as the UK, require banks to be more transparent and give third parties access to customer transaction data- this new phenomenon is known as open banking. Other than just giving customers more transparency when it comes to their finances, open banking also allows payment companies to create better-tailored products, apps and services. As a payment company, one could provide a single portal or app that allows customers to manage all their accounts with different banks. Hence, a major digital payment trend for payment companies is going to be integrating with multiple open banking providers like for example Token.io and TrueLayer, and be an agnostic open banking provider.

Frictionless 3DS2 solutions

As mobile wallets and real-time payments all increase in usership, protecting against fraud is of utmost priority. 3DS2 is a digital payment authentication process that is mandated by the European SCA (strong customer authentication) as a way to safeguard merchants from theft and fraud. In order to comply, merchants are required to incorporate 2 out of 3 of the following authentication elements in their payment flow: 1. something only the user knows like a password or PIN, 2. something only the user possesses like a phone or wearable device, 3. something the user is, like fingerprints or facial recognition. There are two major issues with 3DS2- one is its implementation and the other is the added friction.However, an emerging trend we predict for 2022 is payment companies finding ways to work around these issues. A good frictionless 3DS2 implementation should support merchants, requiring little to no effort from their side. In addition to this, there are various solutions that could reduce friction and subsequently reduce dropouts, if implemented. One such solution is 3DS routing which allows merchants to decide and implement their own 3DS2 strategy. Namely, merchants can choose which transactions they want to pass on to 3DS2, 3DS1, or no 3DS. These features route transactions to the most efficient authentication protocol, taking into account exemptions and other valuable information.

The benefits provided by white-label payment gateways

Let's Connect

Just a few quick details. Our team will reach out to explore how our platform fits your payment stack and objectives.

Talk with one of our payment experts

Ready to elevate your business to new heights? Schedule a call with our experts to discuss your unique needs and uncover tailored solutions. Don’t let questions linger – seize the opportunity to pave your path to success!

Winner !

Best use of data analytics, MPE 2025

Best Payments Orchestration Solution, MPE 2024